[ad_1]

Reasons to take profits in chip stocks are growing, and Texas Instruments (NASDAQ: TXN) is 1 of them. The company’s Q1 results and outlook weren’t horrible, but they didn’t inspire a rally, and more of the same can be expected from the group. Texas Instruments is a diversified chip manufacturer with 6 end markets spanning a broad range of use cases, including consumer electronics, industrial and automotive.

The company says it experienced weakness in all but 1 of its end markets, automotive, and not all chip-makers have that exposure or enough of it to make a difference.

Texas Instruments Outperforms; Guidance Tepid

Texas Instruments had a good enough quarter despite revenue falling 10.8% compared to last year. The revenue beat the Marketbeat.com consensus by a slim margin, and the company’s profit margin was better than expected. The bad news is that revenue is also down sequentially, and the slide may continue in the 2nd quarter. The margin was impacted due to deleveraging and cost increases but fell less than expected. This left the GAAP earnings at $1.85 or $0.07 better than expected to outpace the top-line strength.

Guidance is OK but not a catalyst for higher share prices. The company expects $4.17 to $4.53 billion in revenue, which brackets but has a mid-point below the consensus and opens the door to a sequential decline. Even at the high end of the range, the revenue outlook is down 13% compared to last year, an acceleration of decline from Q1.

The takeaway that management wants investors to leave with is that cash flow remains solid and FCF is robust. The company generated $7.7 billion in cash flow on a TTM basis, with the FCF margin running at 23% of revenue. This fuels repurchases and dividends that are not expected to cease but may not be enough to keep the stock trading where it is.

The Analysts Cap Upside For Texas Instruments

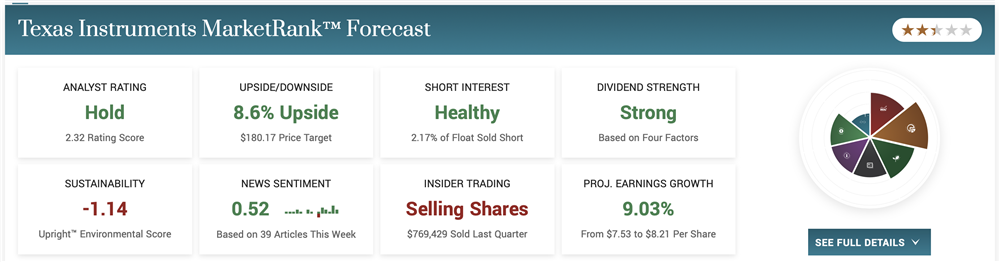

The analysts aren’t bailing on Texas Instruments but have begun to lower their price targets. Marketbeat’s analyst tracking page has picked up 4 price target reductions, impacting the consensus target. The consensus had begun to move higher ahead of the report due to some pre-release target increases, but that trend appears dead on arrival. It’s now capped in the low $ 80s and may move lower over the next few weeks, months and quarters.

“While (Texas Instruments) leads the industry with market share and solid execution, we believe TXN faces challenges with peak margins, high inventories, and a macro slowdown noted by (gross margins) with a potential slowing in China/US into the second half,” said Mizuho analyst Vijay Rakesh wrote in a note.

Capital Returns Are Strong At Texas Instruments

The capital return program is not likely affected at this time. The company’s 2.9% yield and 19-year history of increases appear safe, and share repurchases are also expected. The company repurchased about $103 million during the quarter and should continue quarterly, although the pace may slow. The payout ratio for the dividend is about 48% of the earnings outlook.

The chart is unfavorable to bulls, but a deep decline is not expected either. The market is pulling back following the release but shows some support near the mid-point of a trading range. This level may not hold, but it shows buyers are waiting for a pullback and at a high enough level to allow a deeper pullback without breaking critical support.

[ad_2]

Source link